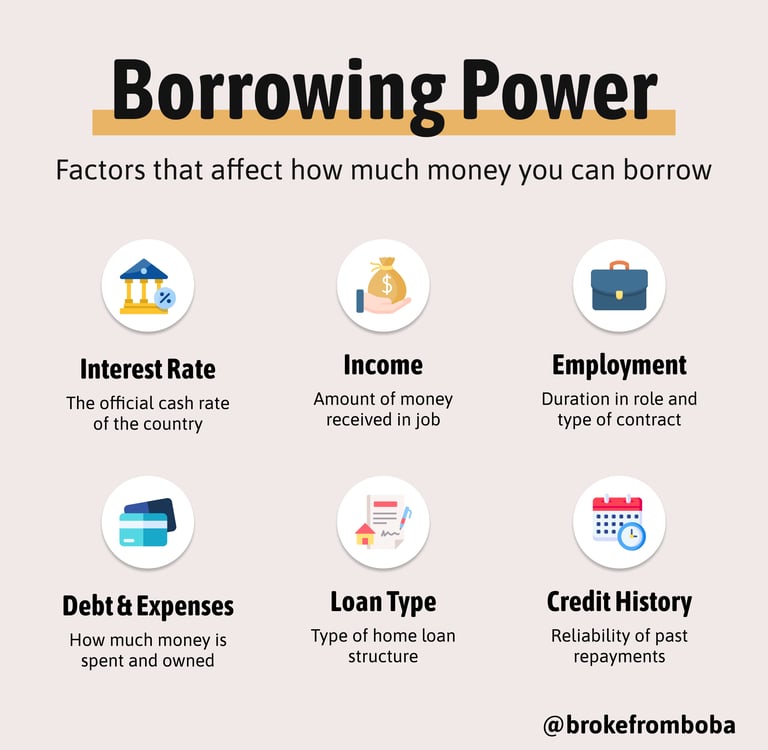

Your borrowing power

Factors that affect how much you can borrow for your mortgage

4 min read

As I prepare to purchase the land of my investment property in the coming months, I reached out to my mortgage broker to initiate the process to borrow the funds required for that purchase.

And I almost couldn't afford it.

I just got a promotion and a salary increase, yet my borrowing power was over $100k less than last year - why was that?

In today's blog, I'll go through the factors that influence how much money can be taken out in the mortgage, and how they affected my personal borrowing power.

FACTOR 1

Country's Interest Rate

The country's interest rate, also referred to as the cash rates, influences the interest rate of financial products (such as higher interest rates on mortgages and savings accounts), as well as someone's borrowing capacity.

If the interest rate increases, the amount of money that needs to be repaid on a mortgage also goes higher. The bank will need to assess someone's ability to meet the increase in repayments, and in Australia, whether they can continue to make repayments if the rates go up by an additional 3%. As a result, borrowing power will reduce so an individual can only borrow what they can afford and have the means to pay back.

Advertisement

FACTOR 2

Employment Income

Income is the amount of money received from one's employment, and is used to understand how much money someone can spend on their mortgage repayments - aka their repayment capacity.

Therefore, if someone's income is high, repayment capacity may also increase, so they can afford to make higher mortgage repayments that comes from borrowing more money. On the flip side, if their income is lower, then they may not be able to borrow as much as their repayment capacity is low.

Advertisement

FACTOR 3

Employment Duration & Type

Given that a length of a mortgage is usually around 30 years, banks want to ensure people are in a stable employment so they can make those repayments throughout that time period. There are two key factors that they look at: duration in role/company and contract type

Duration: How long someone has been working in their current role / company. The longer it has been, the less risk there is. However if they've recently started a new role and/or in a new company (usually less a year or six months in the role), there is greater risk of unemployment due to probationary periods and lack of protection from unfair dismissal.

Contract Type: Permanent employment types without an end date is the most stable form of employment, however other contract types, especially contractors and self employment are risky as there is usually either a defined end date, or income received can be unstable.

The higher the risk from these two factors, the lower an individual's potential borrowing capacity.

Advertisement

Similar to income, the amount of debt and expenses someone has will impact their repayment capacity. The higher the amount of existing debt, bills and spending, the less money they may have leftover to dedicate to the repayments for the mortgage. The less money they available have to spend toward these repayments, the less they can borrow.

FACTOR 4

Debt & Expenses

FACTOR 5

Type of Mortgage

There are two main types of home loans someone can apply for - owner occupied or investment. The amount that can be borrowed via an investment loan is generally higher as the property can make income and can appreciate in value, however the interest rate is also generally higher as it carries more risk where no one may rent the property.

FACTOR 6

Your Credit History

A bank wants to ensure that they are lending money out to those who are reliable and can pay their bills on time. Therefore, they usually review an individual's credit report to assess their reliability before they make a decision on whether the application for a mortgage is approved or declined.

Advertisement

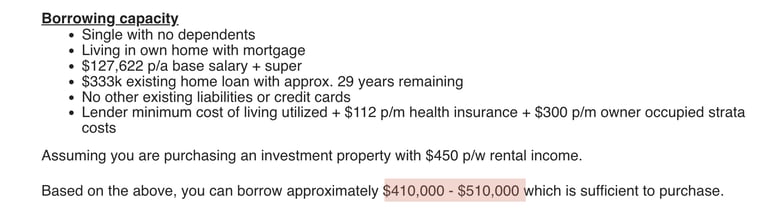

So what happened to my borrowing power?

In December, where I started my new role, a combination of higher interest rates (Factor 1) and my employment (Factor 3) reduced my borrowing power despite a pay rise.

My new job contract was temporary unlike my previous employment which was permanent. Additionally, I've only been in my current role for around 4 months, which was higher risk.

Thankfully I can still borrow just enough to purchase my property but I wasn't prepared for the drastic reduction in my borrowing power so this was a good lesson learnt - and something I hope you can also keep in mind if buying a property is a goal of yours!

MY BORROWING POWER

How my borrowing capacity reduced by over $100k

DEC 22 BORROWING POWER

APR 23 BORROWING POWER

You may be interested in 👀